a 1763 Chinese reproduction of a 1418 map made from Zheng He's voyages

Our firm's China Outbound Investment product was launched in 2008 with a view of providing (to the extent possible) "primary source reconciled data" related to Chinese outbound investments. We did so after hearing so many corporate and institutional investors question the transparency or sources of such data appearing in numerous public sources.

We monitor all Chinese outbound investment across continents, industries and by type/component of investment – both equity and debt. Since the data pre-dates the BRI, this data covers the globe, not just the original 65 OBOR counties, or to the circa 140 countries which are now public (we do not include bank loans by Chinese commercial banks, unless linked to a policy bank).

"To paraphrase Confucius, you must study the past to understand the future."

..... Read more

Click on presentation to open

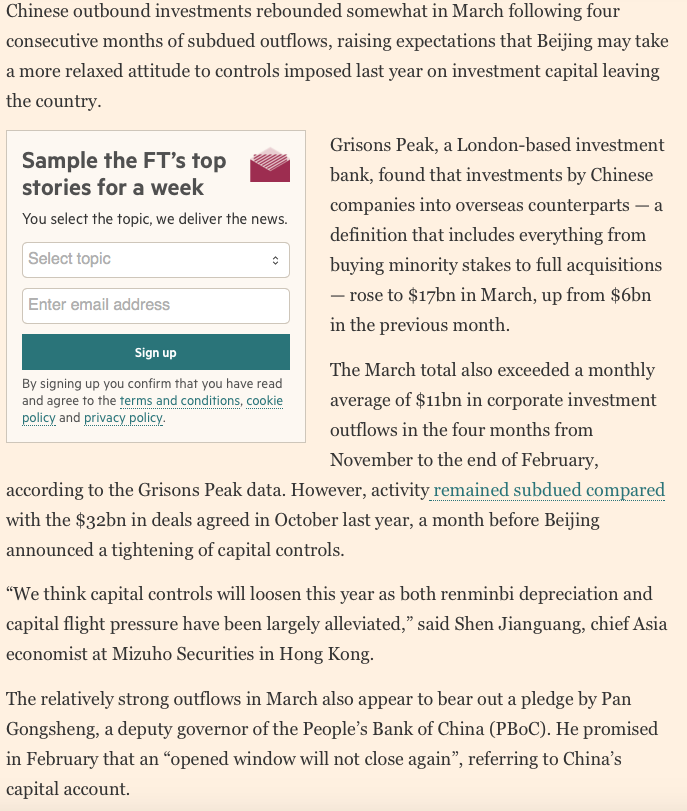

4 April 2017 – China outbound M&A picks up in March after subdued months

Rising M&A activity in March boosts outlook for easing of China’s capital curbs

Belt & Road Initiative: Implications for UK-China Business